We Are Still Living in the Iron Age

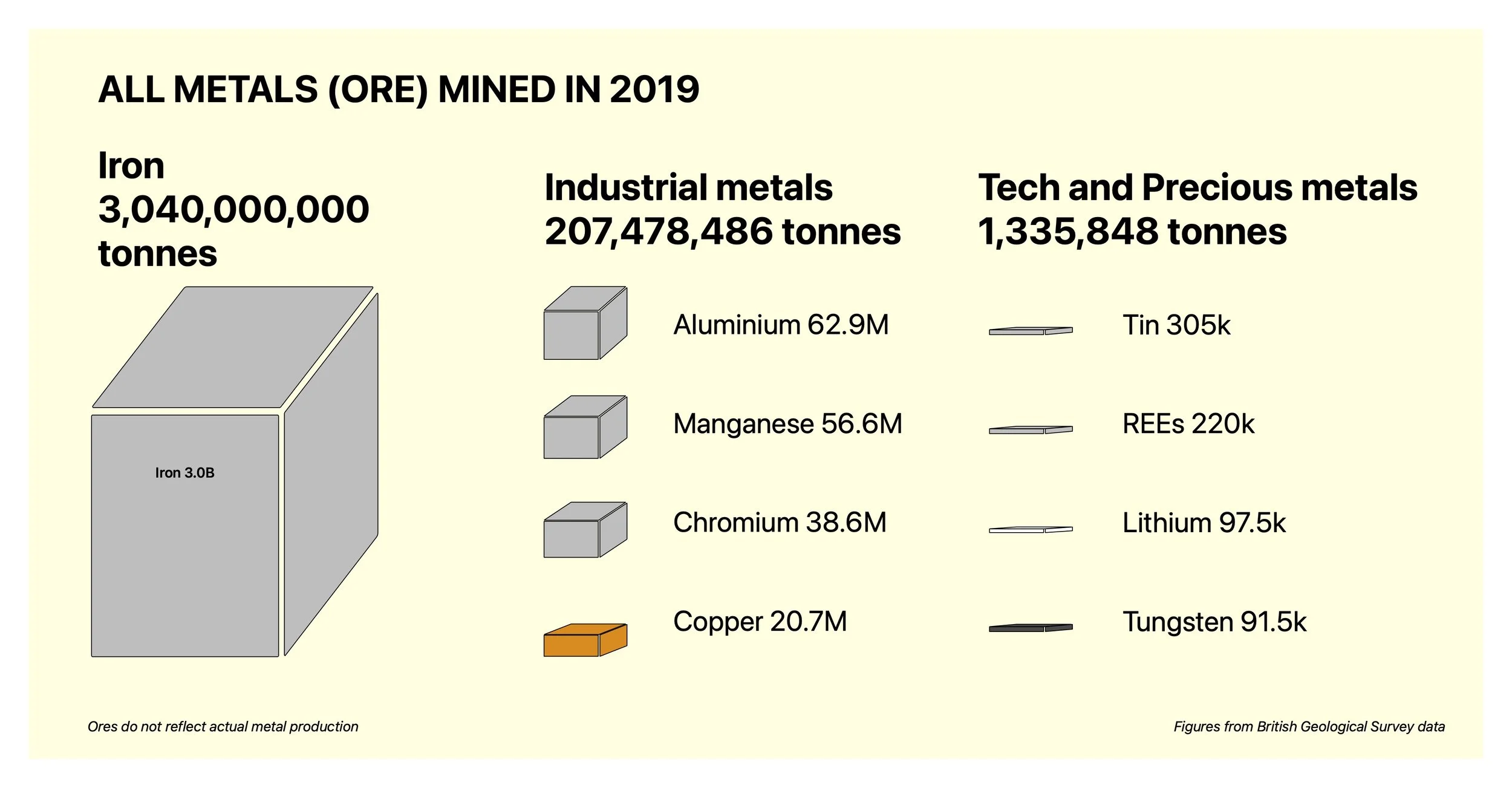

A schematic of the actual figure that appeared in Elements and other materials from the British Geological Survey

I once saw a graphic illustrating the amount of each metal mined globally in 2019. It is perhaps my favourite the British Geological Survey have ever produced. It shows three billion tonnes of iron ore mined in a single year. That is 94% of all metals mined, globally, in one year.

The next largest are aluminium, manganese, and chromium — but these are small fractions. Everything else, including all the metals we talk about most, the critical metals that fill every policy paper and conference agenda, is a rounding error by volume. So the question worth asking is: are we still in the Iron Age?

Human pre-historic eras are usually defined by the dominant material of the era. The Stone Age, the Bronze Age, the Iron Age. After that, human history tends to be framed in terms of cultural or scientific progress: the Classical Era, the Medieval Era, the Renaissance, the Industrial and Modern Eras. But look more closely and you will see that iron never really handed over the baton.

Iron decided much of Classical, Medieval civilisation and continued into the Rennaissance. The sword, the arrowhead, the cannon, the musket barrel. Into the Industrial Era iron became the steam engine, the railway, the ship. In the 20th century it became structural steel, the skeleton of every modern city. Iron usage may have evolved into steel, alloyed with other metals to improve its properties, but the base metal has always been our ferrous friend.

It has dominated human existence since it won its crown in the Iron Age. I think it deserves some appreciation.

The money behind critical minerals

The world is rightly focused on securing new supplies of battery metals: lithium, nickel, cobalt, and a long list of other critical raw materials. We need far more than we currently produce, and that gap needs to be closed. But there is a question that tends to get overlooked: where will the money come from to fund exploration and develop these new resources?

Iron. Three billion tonnes of it.

Iron ore does not sell for a particularly high price per tonne — around $100 at the time of writing. But the volumes at which it is traded are unlike anything else in the world. Steel is a foundational industry in every modern economy for good reason: 98% of all iron ore goes directly into steelmaking. It is the base layer that everything else is built on, closely tied to economic cycles and, in particular, to industrialising countries.

The clearest example is China. From the late 1990s into the 2000s, China industrialised at a rate never seen before, driven by construction on a colossal scale. That created a steel boom that peaked in early 2014.

When China slightly eased its construction pace, the iron ore price collapsed from around $110 a tonne to around $55. Not a slow drift — a collapse, over weeks. China had not stopped growing. It had simply slowed by a couple of percent.

The consequences were far-reaching and long-lasting. The crash did not stay in iron ore. It drained investor sentiment from the entire mining sector: copper, zinc, gold, critical metals. Exploration investment collapsed, and it has taken over a decade to begin to recover.

I sat in a conference room in Toronto a couple of years ago with people who knew the gold market well. The recurring refrain was, "This is the year we will finally see the exploration investment the gold price deserves." It did not happen. It is only now, in 2026, with gold at record prices, that investor confidence has begun to return. Other commodities — zinc, and to a lesser extent copper — have suffered the same.

The critical minerals investment story is real and important. But it is underwritten by the health of the broader mining industry, and the broader mining industry runs on iron.

Iron as a motive

Iron is not just an economic driver. Like oil, it can be a motive for conflict.

It should not go unnoticed that the largest steelmaker in Europe was located in Mariupol, Ukraine. The Azovstal steelworks produced around 30% of Europe's steel. When Russia invaded Ukraine in 2022, one of its objectives was to capture Ukraine's industrial heartland and annex it, making Europe further dependent on Russia. Azovstal became a battleground. President Zelensky eventually instructed the fighters holding the steelworks to surrender, as there was no prospect of relief in the foreseeable future.

The loss of that production hit a steel market that had barely recovered from the shock of COVID-19. Rising steel prices had immediate knock-on effects across mining. A notable example is Drakelands Mine, a world-class tungsten deposit in Devon operated by Tungsten West Limited. It had been working to reopen after closing in 2018, but the steel price rise changed the project economics significantly. It is only now beginning to secure the finance it needs.

Iron shapes geopolitics in ways that rarely make it into the critical minerals conversation.

The future of iron

The new geopolitical paradigm we find ourself in focuses on critical minerals. Until 2022 that was driven by an inevitable energy transition, now it focuses on defence. Despite all the discussion of battery metals and rare earth elements, iron's dominance is not a relic of the past. If anything, the energy transition, and a less peaceful world, reinforces it.

All the infrastructure required to decarbonise the global economy — wind turbines, transmission lines, solar farms, electric vehicle charging networks, grid-scale storage facilities — requires steel to build. Steel is the foundation that net zero depends on. Domestic construction may shift toward lower-carbon alternatives over time. Industrial infrastructure will not. Any argument suggesting that iron will become less important misunderstands what steel is actually used for. Perhaps that is why when the British Geological Survey released their updated Critical Minerals List in December 2024, it included iron - causing many a raised eyebrow.

The associated wealth that the iron ore industry generates is of critical importance to funding the exploration, development, and extraction of the metals that the energy transition and defence industries actually need.

The Iron Age should not be consigned to pre-history. It built the modern world and it will build whatever comes next.

Viva the Iron Age.